Blockchain Basics: Emerging tech is a silver bullet for some, but not a universal solution

April 20, 2020 | Kenyon Briggs

Editor’s note: The opinions expressed in this commentary are the author’s alone. Kenyon Briggs is an attorney at Husch Blackwell in Kansas City. Mindi Giftos and Bob Bowman are partners at Husch Blackwell and contributed to this op-ed, part of a limited series on blockchain sponsored by Husch Blackwell.

[divide]

As blockchain grows in popularity, people continue to look for practical ways to incorporate the technology into their organizations. Some view blockchain as a silver bullet that can conquer any problem. Others view blockchain as a more complicated method for essentially implementing a database, thus offering little more than a solution looking for a problem. So, should your organization use blockchain technology?

The right fit

It is crucial to first determine whether the technical and functional strengths of blockchain’s distributed ledger is the right technology to deliver the desired results. Understanding blockchain’s strengths and limits is key.

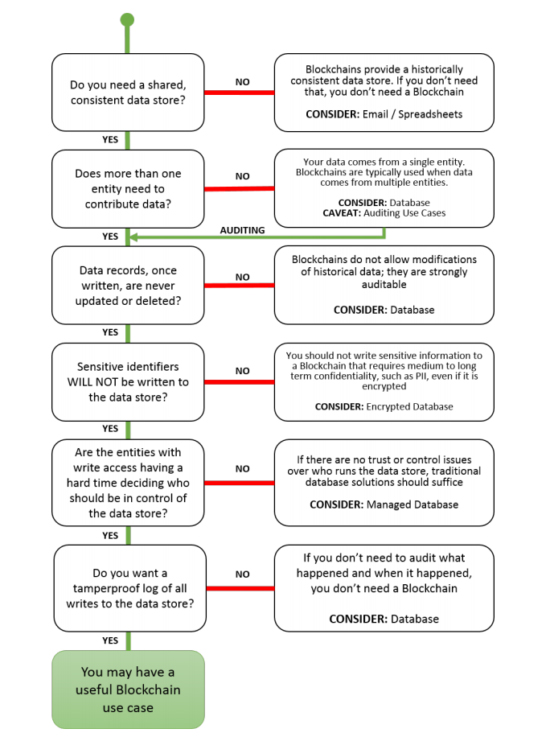

To this end, the U.S. National Institute of Standards and Technology (“NIST”) released a publication in 2018 that, among other things, provides a step-chart to walk someone through the decision on whether implementing blockchain technology makes sense for their organization:

The NIST flowchart is an excellent place to start when determining whether blockchain technology is the right tool for the job at hand. Working through the NIST flowchart can help an organization identify better and worse use cases for blockchain technology. In addition to finding the proper fit, it is important to consider blockchain’s cost. Developing, implementing and supporting blockchain technology can be extremely expensive – estimated costs associated with onboarding and monitoring a private blockchain can easily surpass one million dollars over a five-year span.

Right and wrong fit

An application for which blockchain has shown substantial benefits and applications is a multi-party supply chain, particularly in the food industry.

Kenyon Briggs, Husch Blackwell

Consider a company that wants to help grocery stores by enabling them to: (1) more accurately contain foodborne illness outbreaks and (2) throw out less food as a result of outbreaks. A blockchain could precisely track where every item of produce in a store has been from the time it is planted until the time it arrives in the store. Then, if a store owner learns that E. coli was detected on romaine lettuce originating from the Yuma growing region, for example, the grocery store could pull only the lettuce that passed through that town and leave the rest of the produce on the shelves.

Let’s consider some of the questions on the NIST flowchart. It would be helpful to have information related to the location of produce be accessible by multiple parties because farmers sell romaine lettuce from the Yuma growing region to grocers across the globe. Additionally, multiple parties in the field-to-store supply chain — including growers, harvesters and interstate and even international transporters — would need to separately enter geographic location or transport event information onto the blockchain.

Historical geographic location and transport event data should never need to (and consumers would not want it to) be changed, and the location of produce and transport events are neither sensitive nor private information. Finally, trust between the parties is not always present, so it is crucial that this information be tamperproof. After working through the NIST flow chart, a blockchain may be better equipped to track produce around the globe than a traditional database.

Alternatively, consider a small logistics company in that same supply chain that transports freight across a multi-state area via semi-trucks. The company’s management decides it wants to ditch its existing record keeping method and instead implement a blockchain solution to track when shipments are delivered for quality assurance and internal record keeping purposes.

Working through the NIST flowchart, there are a few reasons why a blockchain may not be the right application for this sort of task. First, if management only wants to track delivery times for quality assurance purposes, there is no need for a shared data store. Additionally, management would be the only group accessing the information, and, in this case, there is no concern as to who is in control of the information. Finally, implementing a blockchain would be much more expensive than keeping a database. In the end, a simple database may be just as effective as a blockchain at tracking the desired information for a fraction of the cost and effort to implement.

Trust

In most cases, blockchain technology is more efficient when there is a lack of trust between the parties using the technology.

For example, a blockchain may make less sense for a small company trying to track its internal information when the only users will be its employees, but would make more sense when multiple parties participate in and must enter information in a long supply chain. This is because a blockchain can reduce the risk of dealing with people who have less of an incentive to be truthful by allowing people to trust the accuracy of the technology itself instead.

However, almost all business transactions already have to account for a lack of mutual trust between parties. Trusted devices and intermediaries like banks, letters of credit, escrow accounts and enforceable contracts are already used to empower global commerce and reduce the risks of doing business. These kinds of business and financial tools already allow distrusting people to do business with each other every day. Although blockchain is capable of replacing some of these trusted intermediaries in a number of applications, businesses will have to consider the unique costs and benefits prior to implementing.

Summary

As the 2020s progress, more and more companies will consider whether blockchain technology is right for them. Businesses will need to analyze blockchain’s strengths and weaknesses and consider the cost to benefit analysis of implementation. Blockchain is not a silver bullet capable of accomplishing any task. But, if implemented to solve the right problem, blockchain technology could give a business a competitive advantage over its competition.

Click here to read the first op-ed in this series, Blockchain Basics: It’s more than a tech buzzword, but how does it actually work?

[divide]

Kenyon Briggs is an attorney in Husch Blackwell LLP’s Kansas City office.

Mindi Giftos is a partner with Husch Blackwell LLP. She is a co-leader of the firm’s Internet of Things (IoT) and Data Privacy, Cybersecurity and Breach Response teams and is the office managing partner of the firm’s Madison, Wisconsin, office.

Robert J. Bowman is a Denver-based partner in Husch Blackwell’s Technology, Manufacturing & Transportation industry group and a co-leader of the firm’s IoT team. He can be reached at bob.bowman@huschblackwell.com

Featured Business

2020 Startups to Watch

stats here

Related Posts on Startland News

Former Kauffman Foundation VP on how to scale via networking

With more than 25 years of leadership experience, Lesa Mitchell knows a thing or two about making — and fostering — valuable connections. Previously the vice president of innovation at the Ewing Marion Kauffman Foundation and a former executive at Marion Labs, Mitchell now is the founder of Networks for Scale, a company that works…