Relationship banking in the digital age: Why businesses should demand a trusted human (backed by tech)

February 5, 2024 | Brian Hoffart

Editor’s note: The opinions expressed in this commentary are the author’s alone. Brian Hoffart, a business banking manager and vice president at nbkc bank, is an experienced Kansas City banker who’s fostered B2B relationships nation-wide for the past 20-years.

The term “relationship banking” has been a core concept of our business for decades.

nbkc bank, Kansas City, Missouri; photo courtesy of nbkc bank

Fundamentally, it asserts that a bank’s relationship with a business is a partnership built on trust, shared objectives, and ongoing communication, with a relationship manager at its center. The relationship manager assures personal connection between the bank and its business client and avails the client of all bank products and services that support its success.

Relationship banking historically has created the basis for mutual benefit — the business client is well-served by a banker who becomes steeped in the company’s business and objectives, becoming a de facto extension of their team; and, in turn, the bank can introduce to the business client a span of relevant products and services, potentially enlarging the bank’s opportunity.

As with most aspects of our business, technology is rapidly reframing the concept of relationship banking. Digital transformation has moved much industry activity online, both with wholly online entrants and physical banks’ adoption of online banking. The resultant shrinking of banking’s physical footprint reduces community presence and the number of business relationship managers.

In this context, how is “relationship banking” redefined? What are the appropriate and realistic expectations for a business-bank relationship? And, really, is it still relevant?

Integrating technology into relationships

The answer is, profoundly, “yes.” The challenge — and the opportunity — is to successfully integrate technology into the relationship banking context. If accomplished, this can enrich a relationship, rather than weaken or replace it.

Technology should simplify routine banking tasks; allow for completion of “pre-work” for human interactions; and provide for two-way visibility of important relationship data for both client and bank. It also enables business clients to engage on their terms. They sometimes will prefer self-service and may value the efficiency and perceived anonymity of digital banking.

Keeping the human touch

The digital/human proportionality and cadence of each relationship likely will be unique. That said, certain elements of the human part of the relationship will be irreplaceable, from the perspective of both the bank and the business client.

The better the bank and client know each other, the greater the chance of mutual success. Therefore, routine transparent communication, inclusive of business clients’ results and strategies and banks’ professional and market insights, will remain critical. It enriches the mutual understanding, and advances the mutual success, of both parties.

Whatever the digital/human construct, banks will rise and fall by “being there” in “moments of truth” … those times when clients’ needs transcend technology platforms or call centers and a reliable, empathetic, trusted and knowledgeable voice is there unfailingly.

Getting there

This all sounds simple, but how do we get there?

First, we need to set realistic, honest relationship expectations. Clients should ask what the bank will offer in terms of human availability and expertise; whether there will be a formal cadence of interaction; and what value-added insights the bank can bring. Banks should be clear on what the business client will be expected to accomplish digitally; what data will be required to provide and how; and the nature and extent of human interaction that can be expected.

In the evolving banking landscape, we should focus on bridging the perceived human/ technology divide, such that each supports the other in cultivating relationships. The more that tasks are accomplished digitally by business clients, the more time is preserved in their interactions with relationship managers for high-value exchange, including company and industry analysis, shared insights and consultation.

Concurrently, ongoing advances in technology, including AI, create the opportunity to enrich the quality of digital interactions so that they, too, contribute to the relationship satisfaction generally associated with empathetic human interaction.

Nothing has changed (while everything has)

nbkc bank, Kansas City, Missouri; photo courtesy of nbkc bank

Businesses should continue to expect — even demand — a trusting, valuable relationship with their bank. That relationship continues to evolve with the intersection of the technological advances and physical retreat of the banking industry. Technology increasingly allows for small businesses to conduct much banking digitally, and over time it will facilitate increasingly substantive components of banking relationships.

That said, the human component of relationship banking remains irreplaceable. With fewer relationship managers industrywide, that component of the relationship will increasingly focus on three things: adding value to small business clients through knowledge and insights; being the doorway into the bank’s full suite of value; and being there, reliably, in the moments where there is no substitute for human interaction, empathy and advocacy.

Relationship banking has evolved with the industry but must remain central to its belief system. No client wants to be just a number at their bank. We are well-reminded that “banking,” without “relationship,” is just, well, banking.

To learn more about how nbkc can support your business banking needs, contact Brian at brian.hoffart@nbkc.com or (913) 383-6497.

Brian Hoffart, a business banking manager and vice president at nbkc bank, is an experienced Kansas City banker who’s fostered B2B relationships nation-wide for the past 20-years. He helps lead nbkc’s Business Solutions, including cash management services and business development initiatives.

Named the strongest large bank in the Kansas City area*, nbkc bank is a diversified banking company known for combining intuitive technology and personal support to create exceptional client experiences. Member FDIC. Equal Housing Lender.

* From an analysis published on April 17, 2023, by the Kansas City Business Journal, comparing all banks with a presence in Kansas City and assets of $1 billion or more. The study used 2022 year-end data from the Federal Deposit Insurance Corporation (FDIC) to evaluate banks on eight metrics which, together, reflect banks’ financial wherewithal.

2024 Startups to Watch

stats here

Related Posts on Startland News

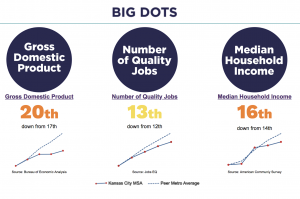

KC Rising update: Kansas City falling short in economic race with peer markets

Bill Gautreaux sounded the alarm with a mixed refrain meant as a KC Rising call to action: “We’re good, but we’re not good enough.” Throughout a recent KC Rising update on the region’s economic growth, Gautreaux and other KC Rising leaders championed Kansas City’s efforts to move the needle, while also lamenting the slow speed…

Kauffman address leaves DC; Execs say the people (not politicians) will revive entrepreneurship

Everyone should have the opportunity to take a risk, achieve success, and give back to their communities through entrepreneurship, Wendy Guillies said. But it’s a collaborative process that begins at home, she noted. “The reality is we all have a part to play in creating a more prosperous national economy and that starts with growing…

No Coast finalists: Trio of startup heavyweights among KC Tech Council award contenders

Updated: Click here for No Coast winners. KC Tech Council released finalists Wednesday for its No Coast awards — a March 8 celebration of trailblazing innovators across the tech industry in Kansas City — which features a handful of startup founders and companies. “These are the folks who went above and beyond in tech,” KC Tech…

Former ECJC exec Melissa Roberts joins Kauffman Foundation grant making team

Everyone has potential if given the right resources, said Melissa Roberts. “Everybody has great ideas if given the right education. Everybody has the potential to be an economic contributor in our society if given the right motivation and support,” she continued. These aren’t her words and values alone, Roberts said. They’re the legacy of Ewing…