Blooom reaches $1 billion in assets under management

September 28, 2017 | Meghan LeVota

")

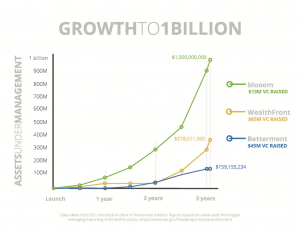

Blooom announced Thursday that the Leawood-based financial tech firm has reached $1 billion in assets under management, becoming the fastest, independent robo advisor to pass that threshold.

Although it’s not the first robo advisor to reach $1 billion, Blooom did so by stretching its dollar much farther than Silicon Valley fintech counterparts, said co-founder Chris Costello.

“This is a source of great pride for us,” Costello said. “Here’s this company from Kansas that with just a tiny fraction of capital reached $1 billion dollars faster than either Betterment or Wealthfront, who have garnered almost all the headlines in the space.”

Blooom helps users grow their 401(k)s using a proprietary online tool that analyzes an individual’s 401(k) and shows its health through a flower in various growth stages. The firm then offers ongoing professional advice on how to allocate funds.

Blooom compared to other robo advisor competition. Data taken from SEC Historical Archive of Investment Advisor Reports based on when each first began managing AUM.

Since its launch in 2013, Blooom has raised more than $13 million, closing an oversubscribed Series B round of $9 million in February. Following the $1 billion milestone, the firm plans to crank up its public relations strategy to garner more national headlines.

Blooom deserves it, Costello said.

“When the story gets out more broadly that there’s this company that’s been flying under the radar that’s accomplished (the $1 billion assets under management milestone) a lot faster than most (robo advisor) companies, I think that’s going to cause more people to pay attention,” he said.

Aside from the milestone being a vehicle to share the Blooom story, it speaks to the firm’s fast-paced progress, Costello said. In 2016, the firm dubbed itself the “fastest-growing robo advisor ever” after reaching $300 million in assets under management in 20 months, years faster than New York City and Silicon Valley Competition.

Costello partially credits this to his decision to grow the firm in the affordable, friendly Kansas City.

“Kansas City has been wonderful to us about following our story,” Costello said. “All of our three co-founders were born and raised in the area and are now raising our families here. We will never move for the company.”

Blooom also taps a larger market than other robo advisors, targeting the average person. About 80 million people in the United States who use a 401k as their primary retirement account, he said.

“The space we’re in is enormous,” Costello said. “The reason why we’re so excited about what we’ve built and what this can turn into is that so many people need this. We’re not just building another service for the wealthy 1 percent. We’re building this for everyone else in America who’s been told that if you don’t have enough money, good luck, figure it out yourself.”

With about 11,000 clients currently, Costello said the company has a long way to go before it taps all 80 million Americans with a 401K.

“We haven’t arrived at the Promised Land yet,” he said. “But, we’re starting to see maybe a path that can get us there. I have a lot of confidence that we are really onto something special.”

In May, Blooom pivoted from a dual-focus on both B2B and B2C channels, laying off nearly a third of its staff. Former Blooom president Greg Smith — who focused on large enterprise partnerships — also resigned from the company.

“We weren’t doing either (B2B and B2C) at 100 percent capacity,” Costello told Startland News in May. “Dividing our attention across individuals and multiple intermediaries muddied — for a whole host of reasons — this singular aim of helping the people who need help the most.”

Blooom was recognized as one Startland News’ Top Startups to Watch in 2017.

2017 Startups to Watch

stats here

Related Posts on Startland News

PopBookings rallies as KC startup looks for its own key hires: ‘We’re back in a big, big way’

After dialing back its event staffing platform’s operations during the pandemic, Kansas City-grown PopBookings is back online in the Midwest — ramping up hiring as it works toward a Series A funding round by year’s end. “Kansas City has a real nurturing feel to it. And this community is why I believe we’ll have our…

$11M renovation in the works for historic hub of Black entrepreneurship; project ties into 18th Street pedestrian mall plans

Editor’s note: The following story was originally published by AltCap, an ally to underestimated entrepreneurs that offers financing to businesses and communities that traditional lenders do not serve. For more than one hundred years, the Lincoln Building has served as a cornerstone of commerce and community in the 18th and Vine district. The historic district —…

MTC’s spring $1.4M investment cycle loops Facility Ally, DevStride into equity deals

Two Kansas City startups are among a handful of Missouri companies receiving a collective $1.4 million in investment allocations through a state-sponsored venture capital program. Facility Ally, led by serial entrepreneur Luke Wade; and DevStride, co-founded by Phil Reynolds, Chastin Reynolds, Aaron Saloff and Kujtim Hoxha; must now complete the Missouri Technology Corporation’s due diligence process…

Kauffman CEO: Foundation’s reset aligns Mr. K’s intent with KC’s needs of the moment

A recently announced strategy refresh for the Ewing Marion Kauffman Foundation will drive the organization’s collective impact in the community — honoring the vision of its namesake while recognizing the challenges Kansas City faces today, said Dr. DeAngela Burns-Wallace. “Mr. K had very distinct philosophies and ideas around how he wanted this work done,” explained…